The Land Where Cash Was King Link to heading

Picture Japan in 2018. Not the anime-filtered Instagram version but the real one. You walk into a ramen shop at midnight, slurp down the best bowl of your life, reach for your phone to tap and pay, and the owner shakes his head slowly, points to a handwritten sign: 現金のみ (Cash only).

This wasn’t some rural backwater. This was Tokyo — one of the most technologically advanced cities on the planet, home to robots, bullet trains, and vending machines that sold everything from hot ramen to neckties. Yet somehow, Japan had resisted the global wave of digital payments with the stubborn determination of a man who refuses to upgrade from a flip phone.

Temple donations? Cash. Train tickets? Mostly cash. A Michelin-starred dinner? Don’t even think about tapping. Japan’s love affair with physical yen wasn’t just habit. it was culture, trust, identity. The crisp, clean bills. The satisfying clink of coins. The feeling that something real had changed hands.

“In 2018, Japan’s cashless payment rate sat at a humble 20% — compared to 90%+ in South Korea and 60%+ in China. Something had to give.”

And then, in October 2018, something absolutely unhinged happened.

The Heist — How PayPay Bribed an Entire Country Into Going Digital Link to heading

SoftBank and Yahoo Japan had a problem. They wanted to launch a mobile payment app in a country that didn’t want mobile payments. The logical, responsible, MBA-approved solution would have been: gradual rollout, thoughtful marketing, patient growth.

Instead, they did something gloriously chaotic. They launched PayPay in October 2018 with a campaign that could only be described as throwing a bag of money off a skyscraper and watching what happens.

The offer: scan the QR code, pay with PayPay, and get 20% cashback instantly on virtually everything. No caps that felt real. No asterisks that mattered. Just: spend money, get money back, repeat.

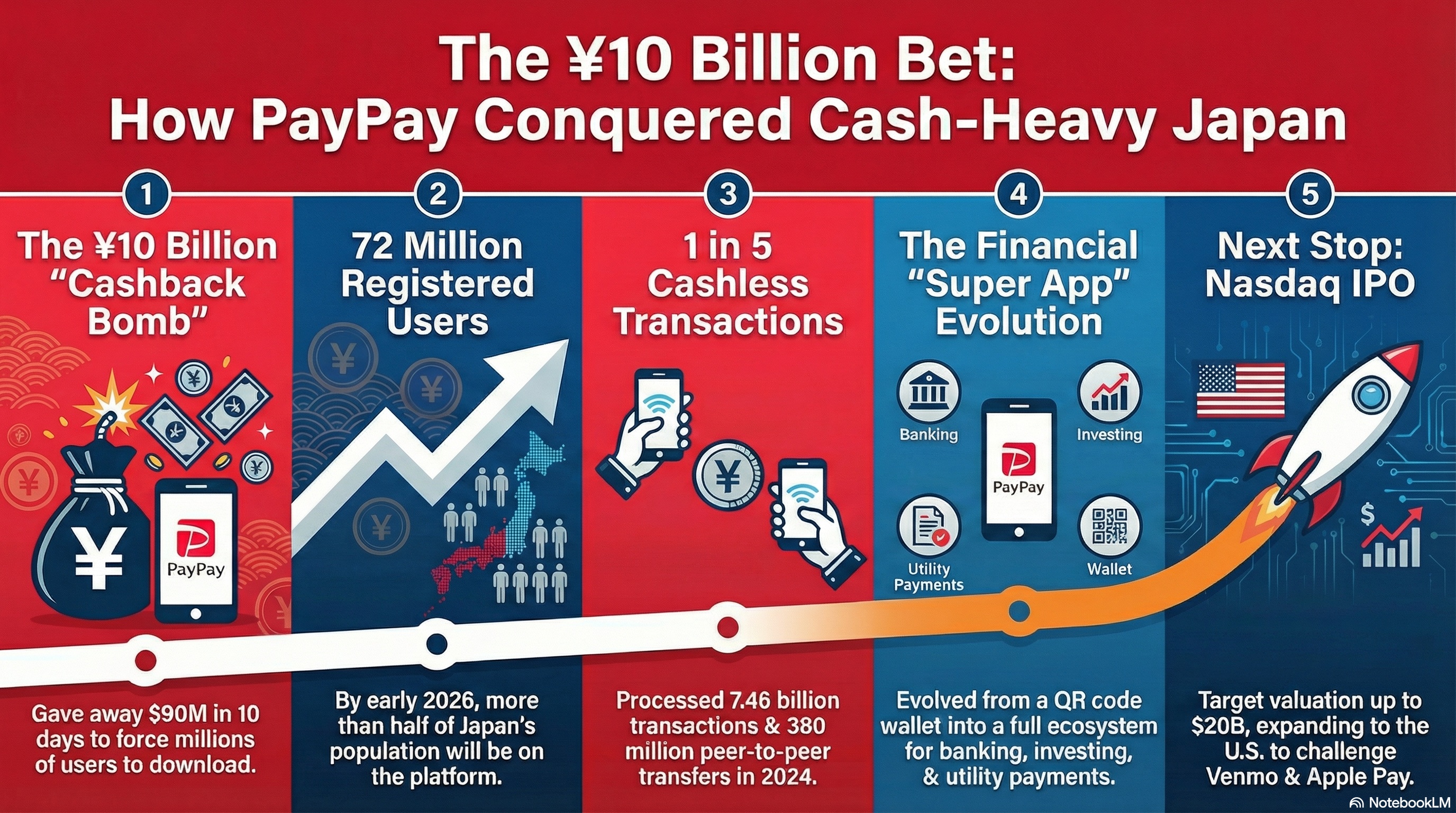

Then came the “10-billion yen” campaign, a ¥10,000,000,000 (roughly $90 million USD) cashback war chest, up for grabs by anyone willing to download an app. Lucky users won 100% cashback on entire purchases. People were buying TVs, cameras, and appliances at major electronics chains, getting the whole amount refunded. Servers crashed. Lines formed outside Yodobashi Camera stores like it was a PS5 launch.

The ¥10 billion was gone in ten days.

“They didn’t build a product and hope people would come. They built a product, lit ¥10 billion on fire, and watched Japan run toward the flames.”

The Cashless Wars — A Battle Royale No One Told You About Link to heading

After the 10-billion heist, every major Japanese tech company smelled blood in the water. What followed in 2019 was one of the most aggressive tech market brawls in Japanese history. a battle so intense, Japanese media literally called it the Cashless Wars.

LINE Pay, backed by Japan’s most popular messaging app. Rakuten Pay, wielding the loyalty points of Japan’s largest e-commerce ecosystem. Merpay, born from Japan’s biggest flea market app. NTT Docomo’s d-Barai. And a half-dozen others. Every week brought a new campaign, a new cashback percentage, a new celebrity endorsement.

Here’s how the scoreboard looked, year by year:

| Year | Milestone |

|---|---|

| Oct 2018 | PayPay launches. The ¥10B cashback bomb drops. Servers buckle. Millions flood in within weeks. |

| 2019 | Tens of millions of users. PayPay wins the cashless wars. LINE Pay and Rakuten fight over scraps. |

| 2020 | COVID hits. Contactless becomes essential, not convenient. PayPay hits ~38 million users. |

| 2024 | 65–68 million registered users. 7.46 billion transactions. 20% of all cashless payments in Japan. |

| July 2025 | Passes 70 million users. 36+ million verified for maximum security features. |

| Early 2026 | Over 72 million registered users — more than half of Japan’s entire population. Trillions in GMV yearly. |

PayPay didn’t just win. It won so decisively that it reshaped the competitive landscape entirely. Today it processes roughly one in five cashless payments in the country — in a market where cashless usage itself exploded from 20% to nearly 40% of all transactions in that same period.

From QR Code to Super App — The Empire Grows Link to heading

Here’s what’s easy to miss: PayPay stopped being a payments app a long time ago.

Today, it’s a financial ecosystem disguised as a wallet. You scan at 7-Eleven for your morning coffee. You pay your electricity bill. You send ¥3,000 to your friend who covered dinner — one of 380 million peer-to-peer transfers processed in 2024 alone. You donate to a temple. You invest in ETFs through PayPay Securities. You hold your emergency fund in PayPay Bank. You earn points on the PayPay Card that fold right back into your digital balance.

Need merchant financing for your small ramen shop? PayPay has a product for that too. The maximum single transaction? ¥1,000,000 yen, tapped with a phone.

It’s the WeChat Pay playbook, executed in one of the world’s most cash-resistant markets. And it worked because PayPay understood something crucial: the first tap was about bribery, but every tap after that had to be about habit. Seamlessness. Speed. The tiny dopamine hit of seeing your balance update in real time.

The Plot Twist — Venmo, Apple Pay, You Have Incoming Link to heading

💥BREAKING: February 2026, PayPay Files for Nasdaq IPO

Ticker: PAYP. Target valuation: north of $10 billion. Some whispers in the investment community say up to $20 billion. The filing confirmed what had been rumored for months — PayPay is going global, and it’s starting with America.

The strategy: team up with Visa, blend QR-code payments with NFC contactless, and launch in markets like California — targeting communities already familiar with QR payments and underserved by existing financial apps.

PayPay isn’t a startup waddling into a new market. It’s a battle-hardened payments giant that spent seven years learning how to convert a population that hated digital payments. It won against dozens of well-funded local competitors. It survived multiple rounds of cashback wars that would have bankrupted lesser companies. And it learned, payment by payment, how to make an app so embedded in daily life that people reach for it before their physical wallet.

The Bottom Line Link to heading

Japan went from 20% cashless to a nation where more than half the population carries a digital wallet called PayPay in under a decade. That ramen shop that used to say 現金のみ? There’s a good chance it has a PayPay QR code on the counter now, right next to the chopstick holder.

It happened because of a ¥10 billion bet that real change sometimes needs an outrageous catalyst. Because a pandemic made contactless feel like survival. Because a company kept adding features until leaving the app felt like leaving money on the table.